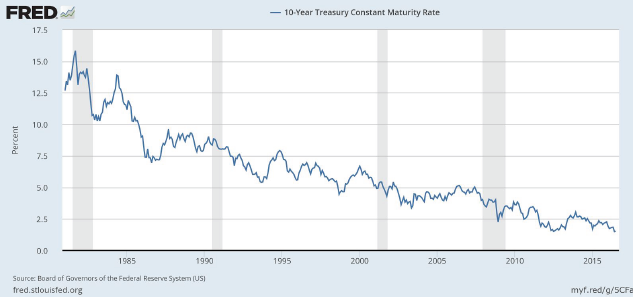

For the last 35 years, interest rates have steadily declined from around 16% to around 1%. Since 2008, our country has been in a near zero interest rate environment. 35 years is a long time. The only market participants who experienced increasing interest rates are retirement age or approaching retirement age. All other market participants have only experienced a slow and steady decrease in interest rates (as seen in the chart below) -- which corresponds to a slow and steady increase in bond prices.

Such extended, one-way price moves tend to produce beliefs like “bonds are safe” or “you can’t lose money in bonds,” etc. While these beliefs may be accurate during a one-way decrease in interest rates with tame inflation, reality is quite a bit more complex.

While the last 35 years have experienced a one-way decrease in interest rates, the preceding 35 years corresponded to a one-way increase in interest rates. During such increases in interest rates, bonds can become worth less. Furthermore, if a bond is held until maturity, the holders will get back their money, but the money they do get back will likely be worth far less than expected, since high interest rates typically correspond to high inflation. (On the figure below, note how high interest rates typically correspond with high inflation, while low interest rates typically correspond with low inflation.)

Andy Haldane from the Bank of England has done an interesting analysis on interest rates. From various sources, he has compiled a 5,000 year history of prevailing interest rates -- from Mesopotamia to today. Over this 5,000 year history, interest rates spent most of their time between about 4% and 6%. More remarkably, our current near zero interest rates are at a 5,000 year low. I guess the Mesopotamians were unwilling to lend for zero return.

As time passes since our recent deflationary event (the Great Recession), I expect interest rates will eventually begin trending towards more historically common levels. Over time, I expect governments will have a hard time restraining spending and money printing, which will result in increased inflation. In the case of the Great Depression, roughly a decade after the depression began, interest rates started their upward march.

Furthermore, over the last few years, a stronger and stronger chorus of investors have piled into lower and lower quality bonds. The reasoning typically follows this rationale: “I used to be able to get a 5% return; now I have to get at least a 4% return”. Instead of stopping to think about whether a 4% return is reasonable in the current 1% return environment, the investor purchases any investment making at least 4%. To achieve these “must have” yields, investors end up grabbing any garbage that promises the required yield (e.g. Greek government bonds for 5%, Petrobras 100-year bonds for 6.85%, etc.). I see such risk-agnostic behavior as concerning, and I see the grab for garbage as very concerning when combined with a 5-millenium low in interest rates.

So, what does all of this mean for stocks?

Since the 1870’s, the average earnings yield (earnings / price) has been about 6% -- which corresponds to a P/E ratio of 16.7. This long-term average earnings yield is close to the 4%-6% long-term average of interest rates. Therefore, a reasonable P/E of the market is something like 1/(interest rate). If interest rates stay in the 1%-2% range for an extended period, stocks could reasonably trade at 50x-100x earnings (2x-4x current prices). Similarly, interest rates could increase to 4% or more without leading to a lasting drop in stock prices. This analysis is at odds with the common media perceptions that increasing interest rates must correspond with a decrease in stock prices and that stocks in general are currently overpriced.

There is one more peculiar implication of a zero interest rate world worth discussing. In the last few years, stock prices of money-losing businesses, which can best be described as toxic sludge, have outperformed the stock prices of money-making businesses.

A business is worth the sum of all future cash flows adjusted for the the time value of money. A dollar tomorrow should be worth less than a dollar today.

Things become very strange as interest rates approach zero. With zero interest rates, cash flow in 30 years is worth the same as cash flow tomorrow. Assuming zero interest rates will last forever allows investors to use this bizarre calculus to justify the price of a money-losing, highly-speculative biotech or social media company because the company “will eventually make a lot of money”.

Because the hypothetical cash flows of a “make money someday business” exist far in the future, the value of the business is very sensitive to interest rate assumptions. Furthermore, with a rise in interest rates, lenders will begin demanding more to loan the money to keep the business operational long enough to reach the hypothetical payday. A small change in rates could rapidly bring the party to an end.

David R. “Chip” Kent IV, PhD

Portfolio Manager / General Partner

Cecropia Capital

Twitter: @chip_kent

Nothing contained in this article constitutes tax, legal or investment advice, nor does it constitute a solicitation or an offer to buy or sell any security or other financial instrument. Such offer may be made only by private placement memorandum or prospectus.